What Were You Thinking?

Half of the S&P 500’s market capitalization now sits in stocks trading above ten times sales. This is a piece about what that number means and what history says happens next. It is not a prediction.

Half of the S&P 500’s market capitalization now sits in stocks trading above ten times sales. This is a piece about what that number means and what history says happens next. It is not a prediction. It is arithmetic. And arithmetic does not care how you feel about it.

«Nowhere does history indulge in repetitions so often or so uniformly as in Wall Street. When you read contemporary accounts of booms or panics, the one thing that strikes you most forcibly is how little either stock speculation or stock speculators today differ from yesterday.»

Edwin Lefevre, Reminiscences of a Stock Operator (1923)

It’s the year 2002.

Sun Microsystems had crashed roughly 90% from its peak.

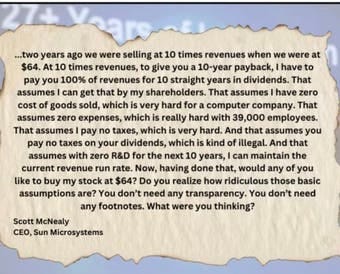

CEO Scott McNealy then gave one of the most remarkable interviews in financial history. He did not blame short sellers. He did not blame the economy. He did not blame his management team. He blamed his investors. For paying ten times sales.

Scott McNealy, CEO of Sun Microsystems, 2002: explaining why paying 10x sales for his stock had been insane

His logic was devastating in its simplicity. At ten times revenues, he explained, to give you a ten-year payback the company would have to pay out 100% of revenues for ten consecutive years in dividends. No cost of goods sold. No operating expenses. No taxes. No R&D. Just hand you every dollar of revenue. And even then, you would need the current revenue run rate maintained for a decade.

«Do you realize how ridiculous those basic assumptions are?» he asked. «You don’t need any transparency. You don’t need any footnotes. What were you thinking?»

McNealy was not speaking hypothetically. He was performing an autopsy on his own stock. Sun never recovered; it was eventually swallowed by Oracle for a fraction of its peak valuation. The company that branded itself «the dot in dot-com» became a footnote.

That was 2002. One company. One cautionary tale that every investor nodded along to and promptly forgot.

Today, 51% of the S&P 500’s market capitalization trades above ten times sales.

S&P 500 sorted by Price-to-Sales ratio. 51% of total market capitalization trades above 10x sales:

Not one stock. Not one sector. Half the index. The same multiple that made a technology CEO call his own shareholders irrational 24 years ago, now applied to half of the most important equity benchmark on the planet.

Different decade. Same math.

The Math Behind 10x Sales

Let me walk you through the arithmetic, because it does not care about narratives.

Take a stock valued at ten times sales. Assume it re-rates to a more normal three times sales over the next decade – which is still a premium. And assume you want a respectable 10% annual return.

For that to work, revenue has to grow roughly eight-fold over ten years. That is about 24% growth, every single year, for ten consecutive years. The multiple compression from 10x to 3x eats more than two-thirds of your gain – so the business has to grow enough to overcome that drag and still hand you a double.

Is that impossible? No. But ask yourself what the base rates are.

McKinsey’s research found that only about 1 in 8 large companies sustains even 10% revenue growth for a decade; for 15%, the odds fall to roughly 1 in 30. And our 10x-sales stock does not need 15%. It needs 24%. The odds of that, at scale, with expanding margins, round to near zero.

The market is currently pricing roughly half the S&P 500 as if it will clear a bar that almost nobody in corporate history has ever cleared.

The base rate says low single digits. The price assumes something like a coin flip.

A bubble does not have to burst. It just has to revert to the base rate. That is all bubbles have ever done.

The Picks-and-Shovels Play on a Revolution That Was Real

In March 2000, one company became the most valuable on Earth.

It made the essential hardware behind the defining technology of its age. Revenue growing 50% a year. The undisputed leader. The picks-and-shovels play on a revolution that was unquestionably real. Wall Street called it the safest way to own the future.

It was Cisco.

The internet was real. The routers were real. The growth was real. At the peak, Cisco traded at roughly 30 times sales and over 150 times earnings, worth about 555 billion dollars. Analysts said it would be the first trillion-dollar company.

Then it fell 90%.

Cisco Systems: peaked near $80 in March 2000. It took until December 2025 – 25 years and 8 months – to see that price again

It took until December 2025 to see that price again. Twenty-five years and eight months to break even – even though the company roughly tripled its revenue over the same period. You did not buy the business. You bought the multiple.

The business won. The stock took 25 years to recover.

Now look at today. The most valuable company on Earth, Nvidia, designs the essential hardware behind the defining technology of its age. The undisputed leader. The picks-and-shovels play on a revolution that is unquestionably real. Wall Street calls it the safest way to own the future.

The internet was real. Artificial intelligence is real too.

That was never the question.

The question is what you pay for a certainty everyone already agrees on.

Interested in arvy’s Database and Portfolio (30 Holdings)?

The «Safest» Stock in the World Just Crossed the Line

If Cisco feels like ancient history and Broadcom like a niche AI bet, here is the example that should genuinely stop you: the most widely held, most beloved, most «safe» stock on the planet. Apple.

Apple now trades at 10.36 times sales – the highest valuation in its entire history. It just crossed the exact line McNealy was talking about.

But here is the part that should stop you cold. McNealy was describing a hypergrowth company. Apple is not. Revenue was $394bn in 2022, $383bn in 2023 — its first decline since 2019 — $391bn in 2024, and roughly $415bn in 2025. Four years. Less than 2% growth a year. Essentially flat.

Apple Price-to-Sales ratio. Now 10.36x — the highest in company history, against a long-term average of 3.6x

Yet over those same four years, when revenue was essentially flat, the stock soared and the price-to-sales multiple nearly doubled.

Read that again. The revenue barely moved. The valuation exploded. Every dollar of the gain came not from Apple selling more — but from investors agreeing to pay more for the same revenue.

That is multiple expansion. It feels like growth. It is not growth. It is sentiment.

Apple’s long-term average price-to-sales ratio is 3.6x. It now sits near 10.4x – almost three times its own norm. For the math to work from here, either Apple suddenly reaccelerates after years of stagnation, or the multiple holds at a record high. Forever.

History says multiples revert. They always do. The only question is whether earnings grow fast enough to cushion the fall.

This is the quiet danger hiding in the «safest» stock in the world. The ultimate quality compounder. A Buffett favourite. A permanent holding. All of that can be true – and you can still lose money for a decade if you buy a flat-growth business at three times its normal price.

Great company. Demanding price. They have never been the same thing.

The Nifty Fifty: When «Buy Quality at Any Price» Ended in Tears

And it is not only about speculative tech. In 1972, the «Nifty Fifty» – Coca-Cola, Disney, McDonald’s, Polaroid, Xerox, the safest blue chips in America – traded at 42 times earnings, with the favourites above 80x.

When 1973 brought inflation, rising rates and recession, they were, in one columnist’s words, «taken out and shot one by one.» Disney fell 87%. Polaroid fell 91% and eventually went bankrupt.

Great companies. Ruinous prices.

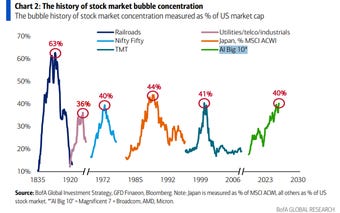

It is a pattern that repeats across every generation – railroads in the 1870s, radio in the 1920s, Japan in 1989, dot-com in 2000, and the AI Big 10 today. Each time, a handful of names swells to an extraordinary share of the whole market.

The history of stock market bubble concentration, measured as % of US market cap. From Railroads (63%) to the Nifty Fifty (40%) to today’s AI Big 10 (40%)

«Buy quality and hold forever» is good advice. «Buy quality at any price and hold forever» has ruined more patient investors than any crash.

It was never one decision. It was always the price.

The Bulls Are Right About the Businesses – and Wrong About the Prices

Let me give the bulls their strongest argument, because it is a good one, and a piece that ignores it is propaganda, not analysis.

The objection goes like this. Today’s leaders are nothing like Sun Microsystems or the profitless companies of the dot-com era. Nvidia, Microsoft, Alphabet, Meta – they are among the most profitable enterprises in history. Fortress balance sheets, real earnings, and record margins that genuinely do justify higher sales multiples: a 30% net-margin business deserves a richer multiple than a 10% one. The quality is real, and quality deserves a premium.

All true. And I agree with most of it.

But notice what it defends: the businesses, not the prices. Cisco was wildly profitable in 2000. So was Microsoft, which still fell 65% and took sixteen years to recover. And the margin argument cuts both ways: margins are the most mean-reverting series in finance. Paying ten times sales while margins sit at all-time highs means stacking two optimistic bets – that the peak multiple holds, and that peak margins persist. Two things must go right, not one.

Profitability protects the company. It does not protect the multiple.

A great business at a great price is the foundation of every fortune. A great business at 25 times sales is a bet that the next decade will be flawless. The first is investing. The second is hope wearing investing’s clothes.

To be clear: I am not saying AI is a bubble in the sense of a fraud or a fad. AI is real. The productivity gains are real. The capex cycle is real – just as the internet was in 2000, just as railroads were in the 1870s. Every one of those revolutions changed the world. And every one of them ruined investors who paid too much for the privilege of being right about the future.

The technology is never the problem. The price is the problem.

When half the index trades above ten times sales, you are not investing in innovation. You are betting that a historically improbable outcome will materialize across hundreds of companies at once. That is not investing. That is faith. And faith, in markets, has a remarkably poor track record.

At arvy, we approach this differently. As I wrote in «Software’s Good Story – and Why It’s Not Good Enough», we walked away from software when the structural uncertainty became permanent. We prefer businesses where the bar is low and the valuation embeds pessimism, not perfection.

Waste Management needs the garbage to keep compounding – a low bar. Safran needs planes to keep flying – a low bar. A chip name at 25 times sales needs a flawless decade – a very high bar.

The price you pay determines the bar the company must clear. We prefer low bars. We sleep better that way.

Scott McNealy Knew

Scott McNealy asked his investors in 2002: «What were you thinking?»

He was being honest. The math at ten times sales was never going to work – not for Sun, not for Cisco, not for the dozens of great companies that crashed 80 to 99% after 2000 and took a generation to recover, if at all.

Today, that same math applies to half the S&P 500. The technology is real. The growth is real. None of that is in dispute.

But the price is the price. And the math is the math.

You just need to ask yourself the one question a technology CEO asked his own shareholders twenty-four years ago, in the wreckage of the last revolution everyone agreed was real.

What were you thinking?

Legal Notice: At the time of publication of this article, the companies mentioned may or may not be portfolio holdings of arvy. Such securities may or may not be included in the portfolio at any point in the future. This document has been prepared solely for informational and marketing purposes and does not constitute an invitation, offer, or recommendation to acquire or sell any financial instruments or to engage in any other transactions. The relevant prospectus and key investor information documents (e.g. PRIIPs KID / Key Information Document) are available free of charge from arvy AG.